In light of news this past week that 3 more condominium projects in the Vancouver area are being forced into receivership, I figured I'd pen my thoughts on why it will have a profoundly negative impact on the Vancouver real estate market. Here is the news story.

First, some debunking, as some people are claiming that because these projects aren't being completed it will put positive price pressure on existing inventory. This is a ridiculous statement for a couple reasons:

1 - the construction workers who were working on those projects are now working on other projects that will complete quicker;

2 - the Sophia, H&H, etc projects will be completed by the receiver at some point;

3 - the number of units we are discussing here is miniscule compared to the total number of households and available housing inventory in Greater Vancouver; and

4 - perhaps only 10% - 20% of the total number of units in question here was destined to be purchased by an actual owner-occupier so there is not a pent up demand for these housing units except for the pent up demand of the speculator to buy a new BMW. See quotes below.

Now lets talk about the main reasons these receivership proceedings will cause such a negative effect. There are two main reasons:

1 - speculators are going to get cold feet as they realize that risk is part of trying to make money in real estate - the days of putting your name down on any pre-sale and selling the assignment or completed condo at a highly inflated price are coming to a close. I figure that this may begin a 'rush for the exits' type of scenario where speculators begin clamouring over each other to get out of the market. This will flood supply at a time when demand is dropping. Econ 101 anyone?

2 - Psychology - this has a huge effect that is immeasurable but as it becomes apparent that the original pre-sale buyers at these projects will have lost their stake in the Vancouver real estate game many will question the wisdom of playing the game at all.

Here is some choice quotes from CBC News:

"When asked about buyers left scrambling to find a home because of construction delays, Eden said he believed most buyers were actually real estate speculators who would not need the homes to live in, and who know pre-sale agreements are always a risk.

The executive director of the Condominium Home Owner's Association, Tony Gioventu, agrees that buying pre-sale condos is a game of speculation.

But he says there are people who buy them who aren't in it for the investment and don't realize the risk.

"Normally, only between five to 30 per cent of pre-sale buyers plan to live in the condo once it's built, estimated Gioventu, "but those who aren't in it for the investment need to protect themselves."

If you are new then check out the comprehensive review post.

Friday, February 29, 2008

Thursday, February 28, 2008

Bubblier than the Bubbliest

Well why not celebrate. Vancouver is the number 2 bubbliest of the bubbly cities in North America and the only one that is yet to pop. At an index value of 276 versus the peak index value for Miami of 279 why not celebrate since Vancouver real estate values will never fall and we will surely have rising prices for another 100 years thus taking over the top spot in short order and retaining that spot for eternity. Champagne will flow in the streets and we will pave them with gold because our real estate will be so precious that the very wealthiest of the wealthy will be the only ones to afford homes in Vancouver.

The fact that Miami prices have fallen 20% since that peak should in no way concern us because you know Vancouver has invincibility to financial turmoil and is a safe haven from all of those messy recessions and credit problems. Just ignore the developments going into receivership and the rampant speculation on pre-sale condos. Just ignore the rapidly growing inventory of unsold existing and new homes. Just ignore the collapse of the forestry, tourism and film industries. Don't worry . . . nothing to see here.

The index is normalized for the US$ / CAN$ exchange rate and is set to an index value of 100 in the year 2000. US prices are from the Case Shiller index values and Vancouver prices are from the REBGV Nominal House Price Index. Click on the chart to make it bigger.

Wednesday, February 27, 2008

Additional January 2008 CMHC Data

The January 2008 CMHC Housing Now report for the Vancouver / Abbotsford area came out today.

Here are some highlights that I found interesting.

Here are some highlights that I found interesting.

Units under construction in (during some stage of being built):

- Entire Vancouver CMA = 25,598

- Vancouver City and Endowment Lands = 6,752

- Surrey / White Rock = 5,090

- Tri-Cities = 3,022

- Burnaby = 3,081

- Langley = 1,159

- Maple Ridge / Pitt Meadows = 1,221

- New West = 1,286

- North/West Vancouver = 1653

Completed but Unabsorbed Units (Vacant/unsold and complete housing units; I'm looking for these numbers to skyrocket this year and next as the number of completions begins to catch up):

- Entire Vancouver CMA = 1,407

- Surrey / White Rock = 430

- Langley = 199

- Maple Ridge / Pitt Meadows = 136

- Vancouver / Endowment Lands = 290

If you are thinking about buying a new home in any of these areas you should be able to put a lot of pressure on the developer to cut you a good discount because they are sitting on a higher level of inventory than they are used to. Of course I think you'll probably get an even better deal if you wait a little while longer.

US Home Prices

This chart is brought to you by the Mess That Greenspan Made and the S&P Case Shiller Index.

My goodness the prices just keep getting lower and lower. Let's just file this one under "You Ain't Seen Nothin' Yet."

Miami - wow. Los Angeles - whew - I'm feeling dizzy. Every single market is declining and many have just started but those steep curves for LA and Miami are something to behold.

Oh how I remember the days when the US housing bubble bloggers were being lambasted for saying that house prices were going to fall - many critics said it couldn't happen and that their area was different. Sweet vindication of their point of view only soured by the knowledge that real families are being financially ruined as we speak.

Coming soon to a city near you.

My goodness the prices just keep getting lower and lower. Let's just file this one under "You Ain't Seen Nothin' Yet."

Miami - wow. Los Angeles - whew - I'm feeling dizzy. Every single market is declining and many have just started but those steep curves for LA and Miami are something to behold.

Oh how I remember the days when the US housing bubble bloggers were being lambasted for saying that house prices were going to fall - many critics said it couldn't happen and that their area was different. Sweet vindication of their point of view only soured by the knowledge that real families are being financially ruined as we speak.

Coming soon to a city near you.

Tuesday, February 26, 2008

Tax-Free Savings Account—A Savings Plan for All Canadians

From the Federal Budget

Savings provide a means by which Canadians can invest in the future and improve their standard of living. For individual Canadians and their families, the accumulation of personal savings brings the security and peace of mind that come with the knowledge that funds will be available in the event of an emergency or for individuals to achieve their goals, such as starting a small business, purchasing a new home or a new car, or taking a vacation. In these ways, savings contribute to a higher standard of living for Canadians.

In support of the economic agenda set out in Advantage Canada, and to improve incentives for Canadians to save, the Government proposes to reduce the taxation of savings through the introduction of a Tax-Free Savings Account (TFSA)—a flexible, registered general-purpose account that will allow Canadians to earn tax-free investment income.

How the Tax-Free Savings Account Will Work

- Starting in 2009, Canadian residents age 18 or older will be eligible to contribute up to $5,000 annually to a TFSA, with unused room being carried forward.

- Contributions will not be deductible.

- Capital gains and other investment income earned in a TFSA will not be taxed.

- Withdrawals will be tax-free.

- Neither income earned within a TFSA nor withdrawals from it will affect eligibility for federal income-tested benefits and credits.

- Withdrawals will create contribution room for future savings.

- Contributions to a spouse’s or common-law partner’s TFSA will be allowed, and TFSA assets will be transferable to the TFSA of a spouse or common-law partner upon death.

- Qualified investments include all arm’s-length Registered Retirement Savings Plan (RRSP) qualified investments.

- The $5,000 annual contribution limit will be indexed to inflation in $500 increments.

The TFSA will provide a flexible savings vehicle for Canadians. Since not everyone is able to save each year, individuals who are unable to contribute $5,000 in a year will be able to carry forward unused contribution room to future years. In addition, in recognition of the fact that most people are likely to have multiple savings objectives at the various stages of their lives—e.g. to purchase a car, home or cottage—the full amount of withdrawals may be re-contributed to a TFSA in the future, to ensure that there is no loss in a person’s total savings room. In recognition of the fact that couples often make their savings decisions and plan for their financial security on a joint basis, individuals may contribute to the TFSA of their spouse or common-law partner, subject to the spouse or partner’s available contribution room.

Canadians will also benefit by being able to use the TFSA to start saving early for a range of needs they may have in the future. Many Canadians may prefer to use a TFSA to save for pre-retirement needs given the absence of tax consequences on withdrawals and the ability to avoid the use of RRSP room for non-retirement savings needs.

The TFSA will also provide seniors with a savings vehicle to meet any ongoing savings needs, something to which they have only limited access once they are over the age of 71 and are required to begin drawing down their retirement savings. Based on current savings patterns, seniors are expected to receive one-half of the total benefits provided by the TFSA.

This is a fantastic new measure for many Canadians. It will benefit low income Canadians the most who may not realize a large benefit from RRSP tax deductions or who have government benefits clawed back because of their income level. It is also my hope that it will encourage investing and saving more than the current lacklustre level.

Monday, February 25, 2008

Observations From the Street

The weather was so nice this weekend, the wife and I decided to take baby mohican for a little drive. No better way to celebrate good weather in the suburbs than burning fossil fuels!

Some interesting observations from driving a little bit off the beaten path.

1) We aren't even close to running out of developable land.

2) There are innumerable new homes under construction in Langley / Surrey.

3) There are many "Development Proposal" signs all over the place for new subdivisions that contain 50 - 500 homes. (Bedford Landing, Milner Heights, Yorkson, Copper Creek, Clayton, and more - these are by developers like Parklane, Adera, Morningstar, Solterra, Foxridge, and lots of other smaller developers)

4) There were hundreds of for sale signs, mostly in new home developments. I assume most of these homes for sale are speculators or developers trying to sell their investment. Very few "sold" signs.

What are your observations from where you were out and about this weekend?

Some interesting observations from driving a little bit off the beaten path.

1) We aren't even close to running out of developable land.

2) There are innumerable new homes under construction in Langley / Surrey.

3) There are many "Development Proposal" signs all over the place for new subdivisions that contain 50 - 500 homes. (Bedford Landing, Milner Heights, Yorkson, Copper Creek, Clayton, and more - these are by developers like Parklane, Adera, Morningstar, Solterra, Foxridge, and lots of other smaller developers)

4) There were hundreds of for sale signs, mostly in new home developments. I assume most of these homes for sale are speculators or developers trying to sell their investment. Very few "sold" signs.

What are your observations from where you were out and about this weekend?

Friday, February 22, 2008

Tolko Shuts Down Interior Mills

Friday, February 22, 2008 03:59 AM

Tolko has announced some temporary curtailments at all four of its Cariboo lumber operations.

A minimum two-week curtailment will begin March 3, affecting more than 1,100 direct and contractor employees at three mills in Williams Lake and one in Quesnel. Nearly 40 million board feet, or one billion board feet on an annual basis, will be removed from the marketplace.

“These decisions are never easy and they are even more difficult when our employees, mills and contractors have performed so well,” says Rob Fraser, General Manager, Cariboo and Alberta Lumber. “Unfortunately, the current economic conditions do not support the continued operation of our mills at their current levels.”

A return to operation for all four mills will depend on market improvements.

2008 has seen Tolko take plenty of action.

January 10th, Tolko announces temporary sawmill curtailment of it’s Manitoba division between January 28 and February 8. 110 employees impacted

February 11th Tolko announces indefinite closure of High Prairie OSB mill 119 employees

February 18th Tolko extends the downtime at two panel operations in Armstrong and White Valley ( near Vernon) 300 workers impacted

February 22nd, Tolko announces curtailment at four Cariboo lumber operations, 1100 direct and indirect workers impacted

In all cases, the curtailments or closures are being blamed on poor market conditions.

More mill closures.

I just have to ask what are the laid off mill workers going to do? Move to Vancouver? Live where? They can't afford to buy any housing here and who would buy their old house anyway. Maybe they could work construction for a year or two and then what? I think its more likely that these people will go work in Alberta in the oil patch and probably retain ownership of their home.

Tolko has announced some temporary curtailments at all four of its Cariboo lumber operations.

A minimum two-week curtailment will begin March 3, affecting more than 1,100 direct and contractor employees at three mills in Williams Lake and one in Quesnel. Nearly 40 million board feet, or one billion board feet on an annual basis, will be removed from the marketplace.

“These decisions are never easy and they are even more difficult when our employees, mills and contractors have performed so well,” says Rob Fraser, General Manager, Cariboo and Alberta Lumber. “Unfortunately, the current economic conditions do not support the continued operation of our mills at their current levels.”

A return to operation for all four mills will depend on market improvements.

2008 has seen Tolko take plenty of action.

January 10th, Tolko announces temporary sawmill curtailment of it’s Manitoba division between January 28 and February 8. 110 employees impacted

February 11th Tolko announces indefinite closure of High Prairie OSB mill 119 employees

February 18th Tolko extends the downtime at two panel operations in Armstrong and White Valley ( near Vernon) 300 workers impacted

February 22nd, Tolko announces curtailment at four Cariboo lumber operations, 1100 direct and indirect workers impacted

In all cases, the curtailments or closures are being blamed on poor market conditions.

More mill closures.

I just have to ask what are the laid off mill workers going to do? Move to Vancouver? Live where? They can't afford to buy any housing here and who would buy their old house anyway. Maybe they could work construction for a year or two and then what? I think its more likely that these people will go work in Alberta in the oil patch and probably retain ownership of their home.

Personal Finance Scenarios

Here are some scenarios for us to consider if one was to purchase a home today with no money down and a 40 year mortgage (a fairly common occurence by all accounts).

Scenario 1: Home Price Appreciates 5% per year for the next five years.

Homebuyer couple buys $350,000 Townhouse in Surrey with 0% down and a 40 year mortgage at a 6% interest rate. They pay the closing costs ($2,500) and CMHC insurance of $12,950. Fortunately for them the home is worth $450,000 in five years when their mortgage comes up for renewal even though they still owe $337,000. edit

Scenario 2: Home Price is flat for 5 years

Homebuyer couple buys $350,000 Townhouse in Surrey with 0% down and a 40 year mortgage at a 6% interest rate. They pay the closing costs ($2500) and CMHC insurance of $12,950 out of pocket. After five years they have only paid down $13,000 of principal and they still owe $337,000. - edit - Not a good situation.

Scenario 3: Home prices decline 30% over 5 years

Same homebuyer couple but after five years their lovely townhouse is only worth $245,000 and they still owe $337,000. What are their options?

They don’t have too many options that make sense as far as I can see besides declaring bankruptcy. I am sure the bank would continue to accept their payments and renew the mortgage but the couple may not be so willing to continue paying for a property that they are so far in the red on. They could walk away and accept 7 years of not having access to credit cards, loans, mortgages but they could pay less money per month and stop the bleeding.

What would be best?

The best thing for them to do in scenarios 2 or 3 is to just rent. In scenario 2 or 3 they could have been paying rent and saving the difference between the rent and the mortgage payment and they would have been much further ahead. In scenario 3 they have essentially ruined themselves financially for a long period of time. Unfortunately I think many of our neighbours in the future will consist of scenario 3 people.

Scenario 1: Home Price Appreciates 5% per year for the next five years.

Homebuyer couple buys $350,000 Townhouse in Surrey with 0% down and a 40 year mortgage at a 6% interest rate. They pay the closing costs ($2,500) and CMHC insurance of $12,950. Fortunately for them the home is worth $450,000 in five years when their mortgage comes up for renewal even though they still owe $337,000. edit

Scenario 2: Home Price is flat for 5 years

Homebuyer couple buys $350,000 Townhouse in Surrey with 0% down and a 40 year mortgage at a 6% interest rate. They pay the closing costs ($2500) and CMHC insurance of $12,950 out of pocket. After five years they have only paid down $13,000 of principal and they still owe $337,000. - edit - Not a good situation.

Scenario 3: Home prices decline 30% over 5 years

Same homebuyer couple but after five years their lovely townhouse is only worth $245,000 and they still owe $337,000. What are their options?

They don’t have too many options that make sense as far as I can see besides declaring bankruptcy. I am sure the bank would continue to accept their payments and renew the mortgage but the couple may not be so willing to continue paying for a property that they are so far in the red on. They could walk away and accept 7 years of not having access to credit cards, loans, mortgages but they could pay less money per month and stop the bleeding.

What would be best?

The best thing for them to do in scenarios 2 or 3 is to just rent. In scenario 2 or 3 they could have been paying rent and saving the difference between the rent and the mortgage payment and they would have been much further ahead. In scenario 3 they have essentially ruined themselves financially for a long period of time. Unfortunately I think many of our neighbours in the future will consist of scenario 3 people.

Thursday, February 21, 2008

January CMHC Data

No time for a longer post today but here are the highlights of the January CMHC Data for the Vancouver area.

Completed and unabsorbed units hit 1407. This is the highest I ever remember - - - so far! The cracks are forming.

Starts were high with 1332 units breaking ground during the month.

Completions were low with only 838 units being finished during January.

Units under construction hit another all time high at 25,195. Ridiculous.

Completed and unabsorbed units hit 1407. This is the highest I ever remember - - - so far! The cracks are forming.

Wednesday, February 20, 2008

Shortage of Wheat

I am long DBA at the time of this post. I am also using the Fidelity Special Situations Fund as an agricultural inflation play.

From CBC News:

Soaring wheat prices have Canadian bakeries struggling, farmers rejoicing and customers digging deeper at the till to pay for their bread and pasta purchases.

The price of flour has been climbing steadily over the last year. The price of flour has doubled in the past two months as weather problems, including two years of droughts in Australia, have depleted wheat stocks to lows not seen since the 1970s. Also contributing to the shortage is the flux of grain farmers switching to other crops, such as canola or corn, that produce biofuels.

"It's a very, very tight situation," said Canadian Wheat Board analyst Bruce Burnett. "World production has been under consumption in the last couple of years, so we have been drawing stocks down … and we've finally hit levels that have made the market very, very concerned about supplies and rightly so."

Burnett said the prices are likely to remain high for at least another 18 months, as it could take up to three years of strong harvests to rebuild the worldwide stocks.

Bakers rising prices

The pricing crunch is affecting bakeries, and their customers, across the country. In Winnipeg, KUB Bakery said its prices need to go up to help cover the rising costs. "We're not going to gouge anyone, we're going to take what we need to stay afloat. Bread is going to have to go up, any product with wheat in it will go up, that's a certainty," Ross Einfeld, the bakery's manager, told CBC News. "I'm sure all bakeries across the board have the same problem. Their flour price has doubled, their ingredient price has doubled. So you're going to see prices increase."

Calabria Bakery, in Scarborough, Ont., is also finding rising flour prices a challenge.

The bakery's Sam Cuzzolino said they use roughly 15 tonnes of flour a month for bread and pizza dough and "as far as the bread side goes, if we're breaking even I'd be amazed at this point." He said if the profits in the 50-year-old business continue to decline, he'll have to consider stopping baking bread altogether.

Mount Pearl, N.L., bakery manager Tom Bennett said bakeries can only swallow flour increases for so long. "It's such a labour intensive thing and really, when you see the cost going up …to pass it on to the customer, it's a very big increase for them to swallow," he said, adding that his customers would be upset if he raised his prices from $1.75 to $2.50 a loaf to help cover the costs.

The rising costs are also shrinking the bottom line at Coleman's grocery store in Mount Pearl, Newfoundland. "From what we were paying a year ago to what we're paying now, it's actually phenomenal," said Tom Bennett, bakery manager. "You wouldn't really think all these different things going on would affect the price of flour here in Mount Pearl, but it has."

Soaring prices have farmers 'optimistic' While bakeries are struggling, the high prices are encouraging for farmers.

Doug Chorney, a wheat farmer near Winnipeg and a member of farmers' group Keystone Agricultural Producers, says he and his colleagues are "very optimistic." "These are the best prices for wheat we've seen in many farming careers, perhaps ever. Everyone is optimistic this is going to be a good year, providing we can produce the crop that hasn't grown yet," he said.

Chorney, who said he has already decided to plant more wheat this year, also said the expected profits may help keep some farmers in the industry. It "may encourage some young farmers to stay on the land and take up farming as a career," he said

And another story:

A massive shortage of wheat on the global market is setting the stage for what some market analysts say could be a "once-in-a-career" windfall.

The stage is being set for record-high prices for Prairie farmers, said Mike Jubinville, a market analyst with ProFarmer Canada, a Winnipeg-based company that helps farmers decide when is the best time to market their commodity.

Wheat supplies in the U.S. are expected to fall to 60-year lows by the end of May, the global inventory of grains continues to decrease as aggressive demand for high quality, high protein wheat is soaring, particularly in Asia, Jubinville told CBC News on Friday.

"In nominal terms, we're looking at prices that have never been achieved before on these various commodities, and obviously that's created a great deal of enthusiasm in the farm community," he said.

The last major rally on wheat was in 1996, Jubinville said, when it sold for $7.50 a bushel. Wheat is currently being traded at $19 a bushel, and the market value of canola has more than doubled. The profit potential for farmers is improving to levels that haven't been seen in decades, he said.

"This is, in my mind, one of those once-in-a-career years, that profits this year can make up for a fair number of bad years," he said.

"It seems like you almost can't go wrong growing any individual crop, and we're just trying to find the ones that have the potential to will make us the most money."

2008 will be the "year of the farmer," he predicted, a dramatic change from recent years, when farmers, plagued by early frost, delayed seeding and drought, seemed to lose money no matter what they grew.

From CBC News:

Soaring wheat prices have Canadian bakeries struggling, farmers rejoicing and customers digging deeper at the till to pay for their bread and pasta purchases.

The price of flour has been climbing steadily over the last year. The price of flour has doubled in the past two months as weather problems, including two years of droughts in Australia, have depleted wheat stocks to lows not seen since the 1970s. Also contributing to the shortage is the flux of grain farmers switching to other crops, such as canola or corn, that produce biofuels.

"It's a very, very tight situation," said Canadian Wheat Board analyst Bruce Burnett. "World production has been under consumption in the last couple of years, so we have been drawing stocks down … and we've finally hit levels that have made the market very, very concerned about supplies and rightly so."

Burnett said the prices are likely to remain high for at least another 18 months, as it could take up to three years of strong harvests to rebuild the worldwide stocks.

Bakers rising prices

The pricing crunch is affecting bakeries, and their customers, across the country. In Winnipeg, KUB Bakery said its prices need to go up to help cover the rising costs. "We're not going to gouge anyone, we're going to take what we need to stay afloat. Bread is going to have to go up, any product with wheat in it will go up, that's a certainty," Ross Einfeld, the bakery's manager, told CBC News. "I'm sure all bakeries across the board have the same problem. Their flour price has doubled, their ingredient price has doubled. So you're going to see prices increase."

Calabria Bakery, in Scarborough, Ont., is also finding rising flour prices a challenge.

The bakery's Sam Cuzzolino said they use roughly 15 tonnes of flour a month for bread and pizza dough and "as far as the bread side goes, if we're breaking even I'd be amazed at this point." He said if the profits in the 50-year-old business continue to decline, he'll have to consider stopping baking bread altogether.

Mount Pearl, N.L., bakery manager Tom Bennett said bakeries can only swallow flour increases for so long. "It's such a labour intensive thing and really, when you see the cost going up …to pass it on to the customer, it's a very big increase for them to swallow," he said, adding that his customers would be upset if he raised his prices from $1.75 to $2.50 a loaf to help cover the costs.

The rising costs are also shrinking the bottom line at Coleman's grocery store in Mount Pearl, Newfoundland. "From what we were paying a year ago to what we're paying now, it's actually phenomenal," said Tom Bennett, bakery manager. "You wouldn't really think all these different things going on would affect the price of flour here in Mount Pearl, but it has."

Soaring prices have farmers 'optimistic' While bakeries are struggling, the high prices are encouraging for farmers.

Doug Chorney, a wheat farmer near Winnipeg and a member of farmers' group Keystone Agricultural Producers, says he and his colleagues are "very optimistic." "These are the best prices for wheat we've seen in many farming careers, perhaps ever. Everyone is optimistic this is going to be a good year, providing we can produce the crop that hasn't grown yet," he said.

Chorney, who said he has already decided to plant more wheat this year, also said the expected profits may help keep some farmers in the industry. It "may encourage some young farmers to stay on the land and take up farming as a career," he said

And another story:

A massive shortage of wheat on the global market is setting the stage for what some market analysts say could be a "once-in-a-career" windfall.

The stage is being set for record-high prices for Prairie farmers, said Mike Jubinville, a market analyst with ProFarmer Canada, a Winnipeg-based company that helps farmers decide when is the best time to market their commodity.

Wheat supplies in the U.S. are expected to fall to 60-year lows by the end of May, the global inventory of grains continues to decrease as aggressive demand for high quality, high protein wheat is soaring, particularly in Asia, Jubinville told CBC News on Friday.

"In nominal terms, we're looking at prices that have never been achieved before on these various commodities, and obviously that's created a great deal of enthusiasm in the farm community," he said.

The last major rally on wheat was in 1996, Jubinville said, when it sold for $7.50 a bushel. Wheat is currently being traded at $19 a bushel, and the market value of canola has more than doubled. The profit potential for farmers is improving to levels that haven't been seen in decades, he said.

"This is, in my mind, one of those once-in-a-career years, that profits this year can make up for a fair number of bad years," he said.

"It seems like you almost can't go wrong growing any individual crop, and we're just trying to find the ones that have the potential to will make us the most money."

2008 will be the "year of the farmer," he predicted, a dramatic change from recent years, when farmers, plagued by early frost, delayed seeding and drought, seemed to lose money no matter what they grew.

Tuesday, February 19, 2008

Economics 101: Opportunity Cost

I have had many discussions with people about how to evaluate the potential purchase of a home and it never fails that the discussion comes around to something like this:

Person: "I'd like to buy a rental property."

Mohican: "Make sure you are buying something that costs less than the rent you will generate."

Person: "I have done the math and if I put 20% down ($100,000) I can buy a house with a basement suite and the rent ($2200/mo) will carry the mortgage ($2200/mo)."

Mohican: "Really, that sounds interesting. Have you factored in taxes, insurance, maintenance, and any unexpected loss of income ($500 / month+)? Additionally, have you factored in the loss of income from your downpayment ($400 / month+)?"

Person: "Hmmmm . . . . I guess I'd have to pay the property taxes and stuff but the house will always go up in value so if I get stuck and can't make those payments I can just sell it."

Mohican: "What about the downpayment? How much could you earn on that every month if you invested it?"

Person: "The money is in a savings account right now and I don't know how much it earns, I think it is 4%."

Mohican: "My suggestion is that you have a look at your math again and assume that you don't have a downpayment. Would this potential purchase look as attractive with 100% financing? Additionally, I suggest that you find a property where the rent will cover ALL of the expenses, including taxes, insurance, maintenance and a buffer for lost income."

Person: "But that is impossible. No property is that cheap."

Mohican: "No property in Vancouver currently has those characteristics but that hasn't always been true nor will it always be true and Vancouver isn't the only place to invest. You are considering purchasing a $500,000 property which yields approximately 4%. This is the same yield as your savings account but with much more risk than a savings account. If I were looking at the same property I would only be willing to pay $330,000 for it, which would give it a yield of about 6%. This increased yield would compensate me for the risks I am taking on by owning the property and for an adequate return on my downpayment."

Person: "But real estate is so powerful because of the leverage component. You are ignoring that."

Mohican: "Yes, I am ignoring it because I can use leverage with all sorts of investments including dividend paying stocks and income trusts where the cash flow would cover my borrowing costs. So to be fair we should evaluate all investments without leverage first so we have a fair comparison and so the investments stand on their own merit."

Person: "I don't understand."

Mohican: "Let's assume we can find a property that yields 4%, which you have done. The price to earnings ratio of that property is 25. We can find a stock with a lower price to earnings ratio that also pays a large enough dividend to pay for our borrowing costs. An initial screen produces dozens of companies that meet these characteristics so based on that we should not purchase the property but the stocks instead."

Person: "But my brother lost his shirt in the stock market and he's made tons of money flipping houses. He owns 5 properties right now and he is buying more all the time."

Mohican: "It sounds like your brother is a speculator/gambler and he'll probably lose his shirt in real estate too. He may have made some money recently but that is no garauntee that the profits will continue. If you are buying for cash flow you should consider the metrics I have put forward but if you are buying for capital gains I can't help you evaluate the investment merits because there are none."

Person: "But real estate always goes up."

Mohican: "No it doesn't. If you are naive enough to believe that you deserve to lose money. Go do some more homework and investigation if you want to be a professional investor. Ameteurs jump in without doing their homework, professionals know all of the knowable facts before jumping in."

Person: "That sounds like work, I think I'll just buy the property."

Mohican: "See you later."

Opportunity cost is the loss of potential gain from the best alternative to any choice. Thus, opportunity cost is the cost of pursuing one choice instead of another. Every action has an opportunity cost. For example, someone who invests $10,000 in a stock denies oneself the interest that one can easily earn by leaving the $10,000 dollars in a bank account instead. Opportunity cost is not restricted to monetary or financial costs: lost time, pleasure or any other benefit that provides utility should also be considered.

Opportunity cost is a key concept in economics because it implies the choice between desirable, yet mutually-exclusive results.

Example

If a city decides to build a hospital on vacant land it owns, the opportunity cost is the value of the benefits forgone of some other thing which might have been done with the land and construction funds instead. In building the hospital, the city has forgone the opportunity to build a sports center on that land, or a parking lot, or the ability to sell the land to reduce the city's debt, since those uses tend to be mutually exclusive. Also included in the opportunity cost would be what investments or purchases the private sector would have voluntarily made if it were not taxed to build the hospital. The total opportunity costs of such an action can never be known with certainty (and are sometimes called "hidden costs" or "hidden losses", what has been prevented from being produced cannot be seen or known). Even the possibility of inaction is a lost opportunity (in this example, to preserve the scenery as-is for neighboring areas, perhaps including areas that it itself owns).

It can also apply to time; one might use a limited vacation time to travel to a place of cultural enrichment or to do household improvements. Thus the two-week road trip might preclude repairing or painting one's house that year. To the vast majority of people, time has value.

Evaluating opportunity cost

Opportunity cost needs not be assessed in monetary terms, but rather can be assessed in terms of anything which is of value to the person or persons doing the assessing (or those affected by the outcome). For example, a person who chooses to watch, or to record, a television program cannot watch (or record) any other at the same time. (The rule still applies if the recording device can simultaneously record multiple programs; there is going to be a limit, and if the number of desired programs exceeds the capacity of the recorder, some of them will not be saved, and thus cannot be seen.) In any case, at the time the person chooses to watch a program, either live or on a recording, they cannot watch something else, and if they are not able to record another program showing at the same time, the opportunity to view it is lost (presuming the particular program is not repeated). Or as another example, someone having a video game can choose to watch a program or play the video game on the TV; they can't do both simultaneously. Whichever one they choose is a lost opportunity to experience the other. Or for that matter, a lost opportunity to engage in some other activity entirely (exercising outdoors, or visiting with family or friends, as merely two examples).

The consideration of opportunity costs is one of the key differences between the concepts of economic cost and accounting cost. Assessing opportunity costs is fundamental to assessing the true cost of any course of action. In the case where there is no explicit accounting or monetary cost (price) attached to a course of action, ignoring opportunity costs may produce the illusion that its benefits cost nothing at all. The unseen opportunity costs then become the implicit hidden costs of that course of action.

Note that opportunity cost is not the sum of the available alternatives, but rather of benefit of the best alternative of them. The opportunity cost of the city's decision to build the hospital on its vacant land is the loss of the land for a sporting center, or the inability to use the land for a parking lot, or the money which could have been made from selling the land, or the loss of any of the various other possible uses—but not all of these in aggregate, because the land cannot be used for more than one of these purposes.

However, most opportunities are difficult to compare. Opportunity cost has been seen as the foundation of the marginal theory of value as well as the theory of time and money.

In some cases it may be possible to have more of everything by making different choices; for instance, when an economy is within its production possibility frontier. In microeconomic models this is unusual, because individuals are assumed to maximise utility, but it is a feature of Keynesian macroeconomics. In these circumstances opportunity cost is a less useful concept.

Friday, February 15, 2008

200,000 Visitors

Good day,

Just thought I'd shout out a quick thanks to everyone of my readers - you - for making the work of blogging quite enjoyable. We reached 200,000 visitors on Saturday last week after 13 months of activity here.

To summarize some observations about the traffic on the blog:

Just thought I'd shout out a quick thanks to everyone of my readers - you - for making the work of blogging quite enjoyable. We reached 200,000 visitors on Saturday last week after 13 months of activity here.

To summarize some observations about the traffic on the blog:

- We get a lot of traffic mid-day during most people's lunch break I assume.

- Most visitors (50%+) use the most common local ISPs - Shawcable and TELUS to visit the blog.

- We also get lots of traffic from financial institutions (RBC, Vancity, TD, etc)

- We also get lots of traffic from Government and school domains and (gc.ca, gov.bc.ca, ubc.ca, bcit.ca)

- Other corporate domains are common as well

- 650 visits per day

- Average visit length of 3 minutes

- It seems that the majority of visitors come direct to the blog without a referral

- Referrals from other local blogs is the next most common way people get here

- Google search results cause an increasing number of visits - especially in the last month or so

Thursday, February 14, 2008

Bill Miller's Comments

This commentary is from Legg-Mason's fund manager - Bill Miller who has the reputation of being the manager with the longest track record of beating the performance of the S&P 500 with the performance of the Legg-Mason Value Trust fund - sold in Canada through CI Investments as the CI Value Trust Fund.

This commentary will be short and to the point:

We had a bad 2007, which followed a bad 2006. Over this two-year span, we underperformed the S&P 500 by around 2000 basis points, our worst showing since the two-year period 1989 and 1990, where we underperformed by 2500 basis points.

In the 25 years since we started the Value Equity mandate in 1982, we have had six calendar years of underperformance. Despite that 19-6 record against the market, all the losses are painful. They are also unavoidable and unpredictable. It would be great if we could figure out how to never underperform.

- - -

About the only advantage of being old in this business is that you have seen a lot of markets, and sometimes market patterns recur that you believe you have seen before. It is not an accident that our last period of poor performance was 1989 and 1990. The past two years are a lot like 1989 and 1990, and I think there is a reasonable probability the next few years will look like what followed those years.

The late 1980s saw a merger boom similar to what we have experienced the past few years and a housing boom as well. In 1989, though, the merger boom came to a halt with the failure of the buyout of United Airlines to be completed. The buyout boom had been fueled by financial innovation. Then it was so-called junk bonds, which had been purchased by many savings and loans in an attempt to earn higher returns. Now it is subprime loans repackaged into structured financial products.

The Fed had been tightening credit to guard against rising inflation, which began to impact housing. By 1990, housing was in freefall, the savings and loans were going bankrupt (as the mortgage companies did in 2007), financial stocks were collapsing, oil prices were soaring in 1990 due to a war in the Middle East, the economy tipped over into recession, and the government had to create the Resolution Trust Corporation to stop the hemorrhaging in the real estate finance markets.

Eerily similar to today, the situation began to stabilize when Citibank got financing from investors from the Middle East. Although the overall market was down only 3% in 1990, we got trounced, falling almost 17%, the result of our large holdings in financials and other stocks dubbed “early cycle,” and which tend to perform poorly as the economy is slowing or when it sinks into recession.

If it were possible to forecast with any degree of accuracy, one might be able to descry a slowing economy from an examination of economic data and perhaps adjust portfolios accordingly. But unfortunately, as I have often remarked, if it’s in the newspapers, it’s in the price. The process works the other way: stocks are a leading indicator, so first they go down and then the data comes in.

In 2007, financial stocks began to decline in early February, before the market corrected in March. They then rallied into May, began a slow decline that culminated in an intermediate bottom in August when the Fed lowered the discount rate, rallied into early October, and then began the precipitous fall that appears to have made a bottom around the third week of January. The decline in financials reflected the freezing up of credit markets that began in August and which still persists, and was followed by a steep drop in consumer stocks in November that also may have seen their worst days now that the Fed has begun to aggressively cut rates. All of this was accompanied by the decline in the housing stocks, which fell almost continuously throughout 2007, ending with a loss of almost 60% on average.

The financial panic got going in earnest as we entered 2008; with global markets all dropping in the double digits or close to it as of this writing. The so-called decoupling thesis, which maintained that non-US and emerging markets and economies would be unaffected by a US slowdown, while not dead (yet), is severely wounded.

The monetary and fiscal authorities have now begun to move with alacrity, with the Fed cutting the funds rate to 3.0% (with likely more to come), and the administration and Congress coming up with a fiscal stimulus package estimated at around $150 billion dollars. Will it be successful? Yes. More precisely, if these measures aren’t enough to free up credit and stimulate spending sufficient to set the economy on a growth path, then additional measures will be taken until that is accomplished. The important point is that the monetary and fiscal policy makers are focused and engaged, and will do what is necessary to stabilize the markets and restore confidence.

This does not mean that the recovery will be swift, or seamless, or without additional trauma. But there will be a recovery, and I think the market abounds with good value. Those values may get even better if the markets get more gloomy, but they are good enough now for us to be fully invested.

I think the market is in for a period of what the Greeks refer to as enantiodromia, the tendency of things to swing to the other side. This is not a forecast, but rather a reflection on valuation.

All of the poorest performing parts of the market, housing, financials, and the consumer sector—with the exception of consumer staples—are at valuation levels last seen in late 1990 and early 1991, an exceptionally propitious time to have bought them. The rest of the market is not expensive, but valuations cannot compare to those in these depressed sectors.

Bonds, on the other hand, specifically government bonds, which have performed so wonderfully as the traditional safe haven during times of turmoil, are very expensive. (In bond land, the only values are in the so called spread product, and there are some quite good values there.) The 10-year Treasury trades at almost 30x earnings1, compared to about 14 times for the S&P 500. The two-year Treasury yields under 2%, and is thus valued at over 50x earnings!

The valuation disparity between Treasuries and stocks is as great today in favor of stocks as it was in favor of Treasuries 20 years ago. Just prior to the Crash of 1987, stocks yielded about 2% (same as today), but traded at over 20x earnings. The 10-year Treasury yielded over 10%, vs. 3.6% today. The two-year Treasury now has a lower yield than the S&P 500, and that is before share repurchases, meaning you can get a greater yield in an index fund than you can in the two-year, and a free long term call option on growth. Even more compelling are financials, where you can get dividend yields about double that of Treasuries, which only adds to their allure, with them trading at price-to-book value ratios last seen at the last big bottom in financials.

I think enantiodromia has already begun. What took us into this malaise will be what takes us out. Housing stocks peaked in the summer of 2005 and were the first group to start down. Now housing stocks are one of the few areas in the market that are up for the year. They were among the best performing groups in 1991, and could repeat that this year. Financials appear to have bottomed, and the consumer space will get relief from lower interest rates.

Oil prices have come down, and oil and oil service stocks are underperforming in the early going. Investors seem to be obsessed just now over the question of whether we will go into recession or not, a particularly pointless inquiry. The stocks that perform poorly entering a recession are already trading at recession levels. If we go into recession, we will come out of it. In any case, we have had only two recessions in the past 25 years, and they totaled 17 months. As long-term investors, we position portfolios for the 95% of the time the economy is growing, not the un-forecastable 5% when it is not. I believe equity valuations in general are attractive now, and I believe they are compelling in those areas of the market that have performed poorly over the past few years. Traders and those with short attention spans may still be fearful, but long-term investors should be well rewarded by taking advantage of the opportunities in today’s stock market.

This commentary will be short and to the point:

We had a bad 2007, which followed a bad 2006. Over this two-year span, we underperformed the S&P 500 by around 2000 basis points, our worst showing since the two-year period 1989 and 1990, where we underperformed by 2500 basis points.

In the 25 years since we started the Value Equity mandate in 1982, we have had six calendar years of underperformance. Despite that 19-6 record against the market, all the losses are painful. They are also unavoidable and unpredictable. It would be great if we could figure out how to never underperform.

- - -

About the only advantage of being old in this business is that you have seen a lot of markets, and sometimes market patterns recur that you believe you have seen before. It is not an accident that our last period of poor performance was 1989 and 1990. The past two years are a lot like 1989 and 1990, and I think there is a reasonable probability the next few years will look like what followed those years.

The late 1980s saw a merger boom similar to what we have experienced the past few years and a housing boom as well. In 1989, though, the merger boom came to a halt with the failure of the buyout of United Airlines to be completed. The buyout boom had been fueled by financial innovation. Then it was so-called junk bonds, which had been purchased by many savings and loans in an attempt to earn higher returns. Now it is subprime loans repackaged into structured financial products.

The Fed had been tightening credit to guard against rising inflation, which began to impact housing. By 1990, housing was in freefall, the savings and loans were going bankrupt (as the mortgage companies did in 2007), financial stocks were collapsing, oil prices were soaring in 1990 due to a war in the Middle East, the economy tipped over into recession, and the government had to create the Resolution Trust Corporation to stop the hemorrhaging in the real estate finance markets.

Eerily similar to today, the situation began to stabilize when Citibank got financing from investors from the Middle East. Although the overall market was down only 3% in 1990, we got trounced, falling almost 17%, the result of our large holdings in financials and other stocks dubbed “early cycle,” and which tend to perform poorly as the economy is slowing or when it sinks into recession.

If it were possible to forecast with any degree of accuracy, one might be able to descry a slowing economy from an examination of economic data and perhaps adjust portfolios accordingly. But unfortunately, as I have often remarked, if it’s in the newspapers, it’s in the price. The process works the other way: stocks are a leading indicator, so first they go down and then the data comes in.

In 2007, financial stocks began to decline in early February, before the market corrected in March. They then rallied into May, began a slow decline that culminated in an intermediate bottom in August when the Fed lowered the discount rate, rallied into early October, and then began the precipitous fall that appears to have made a bottom around the third week of January. The decline in financials reflected the freezing up of credit markets that began in August and which still persists, and was followed by a steep drop in consumer stocks in November that also may have seen their worst days now that the Fed has begun to aggressively cut rates. All of this was accompanied by the decline in the housing stocks, which fell almost continuously throughout 2007, ending with a loss of almost 60% on average.

The financial panic got going in earnest as we entered 2008; with global markets all dropping in the double digits or close to it as of this writing. The so-called decoupling thesis, which maintained that non-US and emerging markets and economies would be unaffected by a US slowdown, while not dead (yet), is severely wounded.

The monetary and fiscal authorities have now begun to move with alacrity, with the Fed cutting the funds rate to 3.0% (with likely more to come), and the administration and Congress coming up with a fiscal stimulus package estimated at around $150 billion dollars. Will it be successful? Yes. More precisely, if these measures aren’t enough to free up credit and stimulate spending sufficient to set the economy on a growth path, then additional measures will be taken until that is accomplished. The important point is that the monetary and fiscal policy makers are focused and engaged, and will do what is necessary to stabilize the markets and restore confidence.

This does not mean that the recovery will be swift, or seamless, or without additional trauma. But there will be a recovery, and I think the market abounds with good value. Those values may get even better if the markets get more gloomy, but they are good enough now for us to be fully invested.

I think the market is in for a period of what the Greeks refer to as enantiodromia, the tendency of things to swing to the other side. This is not a forecast, but rather a reflection on valuation.

All of the poorest performing parts of the market, housing, financials, and the consumer sector—with the exception of consumer staples—are at valuation levels last seen in late 1990 and early 1991, an exceptionally propitious time to have bought them. The rest of the market is not expensive, but valuations cannot compare to those in these depressed sectors.

Bonds, on the other hand, specifically government bonds, which have performed so wonderfully as the traditional safe haven during times of turmoil, are very expensive. (In bond land, the only values are in the so called spread product, and there are some quite good values there.) The 10-year Treasury trades at almost 30x earnings1, compared to about 14 times for the S&P 500. The two-year Treasury yields under 2%, and is thus valued at over 50x earnings!

The valuation disparity between Treasuries and stocks is as great today in favor of stocks as it was in favor of Treasuries 20 years ago. Just prior to the Crash of 1987, stocks yielded about 2% (same as today), but traded at over 20x earnings. The 10-year Treasury yielded over 10%, vs. 3.6% today. The two-year Treasury now has a lower yield than the S&P 500, and that is before share repurchases, meaning you can get a greater yield in an index fund than you can in the two-year, and a free long term call option on growth. Even more compelling are financials, where you can get dividend yields about double that of Treasuries, which only adds to their allure, with them trading at price-to-book value ratios last seen at the last big bottom in financials.

I think enantiodromia has already begun. What took us into this malaise will be what takes us out. Housing stocks peaked in the summer of 2005 and were the first group to start down. Now housing stocks are one of the few areas in the market that are up for the year. They were among the best performing groups in 1991, and could repeat that this year. Financials appear to have bottomed, and the consumer space will get relief from lower interest rates.

Oil prices have come down, and oil and oil service stocks are underperforming in the early going. Investors seem to be obsessed just now over the question of whether we will go into recession or not, a particularly pointless inquiry. The stocks that perform poorly entering a recession are already trading at recession levels. If we go into recession, we will come out of it. In any case, we have had only two recessions in the past 25 years, and they totaled 17 months. As long-term investors, we position portfolios for the 95% of the time the economy is growing, not the un-forecastable 5% when it is not. I believe equity valuations in general are attractive now, and I believe they are compelling in those areas of the market that have performed poorly over the past few years. Traders and those with short attention spans may still be fearful, but long-term investors should be well rewarded by taking advantage of the opportunities in today’s stock market.

Wednesday, February 13, 2008

Can you afford to retire?

It's RRSP season and I'm really busy so I thought I'd post on retirement planning since it is the topic that is so popular this time of year.

How much do you need to save in order to afford the lifestyle you want in retirement?

What rate of return do you need from your investments in order to make your retirement goal?

What is a comfortable retirement for you?

Here are a couple places to start if you don't know the answers to these questions:

http://finance.sympatico.msn.ca/SavingsDebt/savings_calculator.aspx

http://www.fiscalagents.com/Yahoo/calcs/retplan.shtml

How much do you need to save in order to afford the lifestyle you want in retirement?

What rate of return do you need from your investments in order to make your retirement goal?

What is a comfortable retirement for you?

Here are a couple places to start if you don't know the answers to these questions:

http://finance.sympatico.msn.ca/SavingsDebt/savings_calculator.aspx

http://www.fiscalagents.com/Yahoo/calcs/retplan.shtml

Tuesday, February 12, 2008

Negative Equity - Coming Soon to a Home Near You

Third of recent buyers owe more than home's value: report

Tue Feb 12, 9:48 AM ET

More than 30 percent of U.S. homeowners who bought in the last two years owe more on their mortgage than their house is currently worth, a housing market research company said on Tuesday.

The housing market peaked in most U.S. markets in the last two years. Of home buyers in 2006, 39 percent of those with a median 10 percent down payment now have negative home equity similar to 30 percent of those who purchased in 2007, said online company Zillow in its quarterly home value report.

Overall, only 3 percent of those who purchased in 2003, and less than 1 percent of all homes in the United States regardless of when they were purchased, have negative equity. At the same time, U.S. home prices fell 3 percent last year from 2006. Condos and single-family residence values dropped 7.4 percent and 5.5 percent, respectively, the report said.

Nationwide in last three months of 2007, all home types fell 3.3 percent from the third quarter and 3 percent year-over-year. "With consecutive declines over the past five quarters, we haven't seen the housing market bottom yet, and it may very well get worse before things get better," said Stan Humphries, Zillow vice president of data and analytics.

"Even many markets that have been largely insulated from recent declines, like some in the Pacific Northwest, reported notable value declines in the fourth quarter," he added. Home values overall fell in the fourth quarter of 2007, to around $224,890, while condominiums posted the largest year-over-year drop, down 7.4 percent to around $229,017.

The fourth-quarter Zillow report taps data for the nation and 125 metro markets, covering 67 million homes. (Reporting by Chris Sanders; Editing by Jonathan Oatis)

Monday, February 11, 2008

Forestry Sector News

Some facts (2005 data):

- Logging operations employ 21,600 people in BC

- Logging and silviculture accounts for 2.9% of GDP

- Wood Product manufacturing employs 43,600 people in BC

- Wood Product manufacturing accounts for 3.6% of GDP

- Pulp and Paper manufacturing employs 12,300 people in BC

- Pulp and Paper manufacturing accouts for 1.5% of GDP

TimberWest to permanently close Elk Falls sawmill

TimberWest Forest Corp. has announced that it will permanently close the Elk Falls sawmill in Campbell River, B.C. The last full operating shift will be May 9. - 2/8/2008

Interfor's Adams Lake mill taking downtime

Interfor's Adams Lake sawmill and planer in Chase, B.C., were down this week and are scheduled to remain down the week of January 28, due to market conditions. The downtime will be re-evaluated early next week, according to a company spokesman. - 1/25/2008

Canfor to indefinitely close OSB, plywood mills

Canfor has announced plans to close its Polarboard OSB mill and Tackama plywood mill, both in Fort Nelson, B.C., for an indefinite duration due to market conditions. The mills will be closed once existing log inventories are utilized and finished products are shipped. This is expected to occur in April for the Tackama mill and during the summer for the Polarboard operation. The Tackama mill has an annual capacity of 270 million square feet (3/8-inch basis) of plywood, and the Polarboard mill has an annual capacity of 640 million square feet of OSB. - 1/18/2008

Tolko schedules downtime

Tolko has announced plans to take a temporary, two-week curtailment at the Manitoba Solid Wood Division between January 28 and February 8. "High log costs, the continued weakening of market conditions, and difficulty managing within the Softwood Lumber Agreement's quota restrictions are the three main factors which led to this decision," said Dave Neufeld, plant manager. The downtime will reduce the mill's production by 6.5 million board feet. The division expects to return to production on February 11. - 1/16/2008

Two AbitibiBowater sawmills shut down indefinitely

Two AbitibiBowater sawmills and two planers, all in Mackenzie, B.C., went down for an indefinite duration beginning January 11. Market conditions were cited. The two mills have an annual production capacity of 475-500 million board feet. - 1/15/2008

Winton Global extends downtime to March

Winton Global Lumber Ltd., Prince George, B.C., has extended the Christmas shutdown of all operations until mid- to late March. Market conditions, and flooding due to an ice jam on the Nechako River, were cited. Upon resumption of operations in March, the sawmill and planer may only operate until the log deck has been utilized and rough lumber processed and shipped. At that time, the operations would be subject to another temporary shutdown. The inventory of logs at the sawmill will allow for about three months of operations. - 1/15/2008

Tembec to reduce production

Tembec has announced plans to cut production via a reduced work week at its sawmill and planer in Elko, B.C., beginning January 14. The company also will reduce production at its Canal Flats sawmill starting the week of January 21. Over the next three months, Tembec will take the equivalent of three weeks of production downtime, through reduced shifts at the mills. The curtailments will reduce production by about 24 million board feet. Market conditions and exchange rates were cited. - 1/14/2008

Well I sure am glad we have a NEW ECONOMY in British Columbia that isn't dependant on the messy forestry sector for a big part of our economic output. The retail sector and the darling real estate sector combined with the uplifting effects of hosting a two week long sporting event in two years will replace this antiquated business of cutting down trees and sawing them into usable lumber to build things with. In the past, the effects of a forestry industry in its death spiral would have had disastrous consequences on our provinces economy. I'm sure glad that those baristas at Starbucks, the framers building lousy overpriced houses, and the real estate agents who consume the coffee and buy the houses will keep our economy afloat. Clearly real estate agents are the most beneficial purveyors of wealth in our provincial economy.

- Logging operations employ 21,600 people in BC

- Logging and silviculture accounts for 2.9% of GDP

- Wood Product manufacturing employs 43,600 people in BC

- Wood Product manufacturing accounts for 3.6% of GDP

- Pulp and Paper manufacturing employs 12,300 people in BC

- Pulp and Paper manufacturing accouts for 1.5% of GDP

TimberWest to permanently close Elk Falls sawmill

TimberWest Forest Corp. has announced that it will permanently close the Elk Falls sawmill in Campbell River, B.C. The last full operating shift will be May 9. - 2/8/2008

Interfor's Adams Lake mill taking downtime

Interfor's Adams Lake sawmill and planer in Chase, B.C., were down this week and are scheduled to remain down the week of January 28, due to market conditions. The downtime will be re-evaluated early next week, according to a company spokesman. - 1/25/2008

Canfor to indefinitely close OSB, plywood mills

Canfor has announced plans to close its Polarboard OSB mill and Tackama plywood mill, both in Fort Nelson, B.C., for an indefinite duration due to market conditions. The mills will be closed once existing log inventories are utilized and finished products are shipped. This is expected to occur in April for the Tackama mill and during the summer for the Polarboard operation. The Tackama mill has an annual capacity of 270 million square feet (3/8-inch basis) of plywood, and the Polarboard mill has an annual capacity of 640 million square feet of OSB. - 1/18/2008

Tolko schedules downtime

Tolko has announced plans to take a temporary, two-week curtailment at the Manitoba Solid Wood Division between January 28 and February 8. "High log costs, the continued weakening of market conditions, and difficulty managing within the Softwood Lumber Agreement's quota restrictions are the three main factors which led to this decision," said Dave Neufeld, plant manager. The downtime will reduce the mill's production by 6.5 million board feet. The division expects to return to production on February 11. - 1/16/2008

Two AbitibiBowater sawmills shut down indefinitely

Two AbitibiBowater sawmills and two planers, all in Mackenzie, B.C., went down for an indefinite duration beginning January 11. Market conditions were cited. The two mills have an annual production capacity of 475-500 million board feet. - 1/15/2008

Winton Global extends downtime to March

Winton Global Lumber Ltd., Prince George, B.C., has extended the Christmas shutdown of all operations until mid- to late March. Market conditions, and flooding due to an ice jam on the Nechako River, were cited. Upon resumption of operations in March, the sawmill and planer may only operate until the log deck has been utilized and rough lumber processed and shipped. At that time, the operations would be subject to another temporary shutdown. The inventory of logs at the sawmill will allow for about three months of operations. - 1/15/2008

Tembec to reduce production

Tembec has announced plans to cut production via a reduced work week at its sawmill and planer in Elko, B.C., beginning January 14. The company also will reduce production at its Canal Flats sawmill starting the week of January 21. Over the next three months, Tembec will take the equivalent of three weeks of production downtime, through reduced shifts at the mills. The curtailments will reduce production by about 24 million board feet. Market conditions and exchange rates were cited. - 1/14/2008

Well I sure am glad we have a NEW ECONOMY in British Columbia that isn't dependant on the messy forestry sector for a big part of our economic output. The retail sector and the darling real estate sector combined with the uplifting effects of hosting a two week long sporting event in two years will replace this antiquated business of cutting down trees and sawing them into usable lumber to build things with. In the past, the effects of a forestry industry in its death spiral would have had disastrous consequences on our provinces economy. I'm sure glad that those baristas at Starbucks, the framers building lousy overpriced houses, and the real estate agents who consume the coffee and buy the houses will keep our economy afloat. Clearly real estate agents are the most beneficial purveyors of wealth in our provincial economy.

Thursday, February 07, 2008

BurnRate.ca - Do you spend too much?

From CBC News.

More than half of Canadians under 50 spend their disposable incomes without thinking about their financial futures, suggests a study released Thursday. I encourage you to go to http://www.mackenziefinancial.com/en/burnrate/index.html to check out the resources that Mackenzie has setup. In particular the videos are quite funny and may hit a little close to home for some.

Researchers asked 1,169 adult Canadians to complete an online survey of 10 questions on their spending habits that could be answered yes or no. The polling was conducted by Decima Research in December.

A respondent who answered yes to up to three of the questions was considered a controlled spender, while anyone who answered yes to four to six of the questions showed overspending tendencies. Anyone answering yes to seven or more questions was categorized as an overspender.

The study found Canadians are busy shoppers, with 45 per cent hitting the stores, not including for groceries, twice or more weekly. More than half of Canadians admitted to being impulse buyers, while 37 per cent of respondents under 50 and 22 per cent of those over 50 said they have hidden purchases or told someone they paid less for an item than they actually did.

Many Canadians said they rely on retail therapy for a pick-me-up, with 60 per cent of those under 50 and 47 per cent over 50 making purchases to make themselves feel better.

And when they're spending, almost half of Canadians use their credit cards to buy something when they don't have enough money in their bank accounts to pay for it.

Young, middle-aged not planning for future

Thirty-seven per cent of Canadians said they are not planning financially for the future. Forty per cent under 50, and 21 per cent over 50, said they focus on spending today rather than making a budget.

Sunghwan said he was surprised by the findings, especially "the great divide between under 50 versus over 50 people."

On average, Canadians under 50 answered yes to 4.35 of the test questions, compared to 2.88 for those 50 and above. Only five per cent of respondents over 50 were considered overspenders.

The findings suggest younger and middle-aged people "tend to basically spend money without thinking about their financial future," Sunghwan told CBCNews.ca, adding they "don't seem to appreciate the fact that the retirement age is quickly approaching and this realization often comes as they reach the age of 50, but it's way too late.

"We need to really encourage younger Canadians to start saving money and to develop a healthy habit of saving and investing as early as possible."

Curb your spending

Sunghwan said the study showed a concerning pattern of young and middle-aged people focused "on now rather than the future."

He said the most important changes people can make to improve their spending habits and start saving for the future are creating budgets and using cash instead of credit, because "people tend to feel greater pain when they hand over cash than when they are using a credit card."

He also recommended that Canadians arrange for a set amount of pay be automatically transferred to their savings and investing accounts.

"This way you save first and use the remaining money as necessary, instead of the other way around," he said. And for the impulse shoppers, he said, "Try to walk away for at least 24 hours if you're about to buy something on impulse… during this 24 hours, you are likely to realize that the things you are about to purchase on impulse are not really that important."

More than half of Canadians under 50 spend their disposable incomes without thinking about their financial futures, suggests a study released Thursday. I encourage you to go to http://www.mackenziefinancial.com/en/burnrate/index.html to check out the resources that Mackenzie has setup. In particular the videos are quite funny and may hit a little close to home for some.

- Have you gone shopping and/or bought things to make yourself feel better?

- Have you spent money in your account near the end of a pay period, because you knew you were about to get paid again?

- Have you hidden purchases from family or friends, or told someone you paid less for something than you actually did?

- Have you bought things you wanted, without considering the longer-term impact of the cost on your personal finances?

- Have you entertained family or friends at home or at a restaurant more than you could afford?

- Have you used your credit card to buy something when you didn't have enough money in your bank account to pay for it?

- Have you avoided looking at your bank account or balance because you were concerned about how much money you've spent?

- Have you regularly bought things on the spur of the moment?

- Have you gone shopping (not including grocery shopping) two or more times a week?

- Have you focused on spending today ahead of creating a budget or financial plan for the future?

Researchers asked 1,169 adult Canadians to complete an online survey of 10 questions on their spending habits that could be answered yes or no. The polling was conducted by Decima Research in December.

A respondent who answered yes to up to three of the questions was considered a controlled spender, while anyone who answered yes to four to six of the questions showed overspending tendencies. Anyone answering yes to seven or more questions was categorized as an overspender.

The study found Canadians are busy shoppers, with 45 per cent hitting the stores, not including for groceries, twice or more weekly. More than half of Canadians admitted to being impulse buyers, while 37 per cent of respondents under 50 and 22 per cent of those over 50 said they have hidden purchases or told someone they paid less for an item than they actually did.

Many Canadians said they rely on retail therapy for a pick-me-up, with 60 per cent of those under 50 and 47 per cent over 50 making purchases to make themselves feel better.

And when they're spending, almost half of Canadians use their credit cards to buy something when they don't have enough money in their bank accounts to pay for it.

Young, middle-aged not planning for future

Thirty-seven per cent of Canadians said they are not planning financially for the future. Forty per cent under 50, and 21 per cent over 50, said they focus on spending today rather than making a budget.

Sunghwan said he was surprised by the findings, especially "the great divide between under 50 versus over 50 people."

On average, Canadians under 50 answered yes to 4.35 of the test questions, compared to 2.88 for those 50 and above. Only five per cent of respondents over 50 were considered overspenders.

The findings suggest younger and middle-aged people "tend to basically spend money without thinking about their financial future," Sunghwan told CBCNews.ca, adding they "don't seem to appreciate the fact that the retirement age is quickly approaching and this realization often comes as they reach the age of 50, but it's way too late.

"We need to really encourage younger Canadians to start saving money and to develop a healthy habit of saving and investing as early as possible."

Curb your spending

Sunghwan said the study showed a concerning pattern of young and middle-aged people focused "on now rather than the future."

He said the most important changes people can make to improve their spending habits and start saving for the future are creating budgets and using cash instead of credit, because "people tend to feel greater pain when they hand over cash than when they are using a credit card."

He also recommended that Canadians arrange for a set amount of pay be automatically transferred to their savings and investing accounts.

"This way you save first and use the remaining money as necessary, instead of the other way around," he said. And for the impulse shoppers, he said, "Try to walk away for at least 24 hours if you're about to buy something on impulse… during this 24 hours, you are likely to realize that the things you are about to purchase on impulse are not really that important."

Wednesday, February 06, 2008

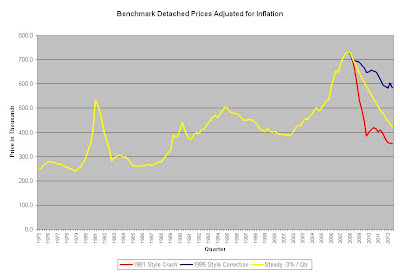

Correction Scenarios