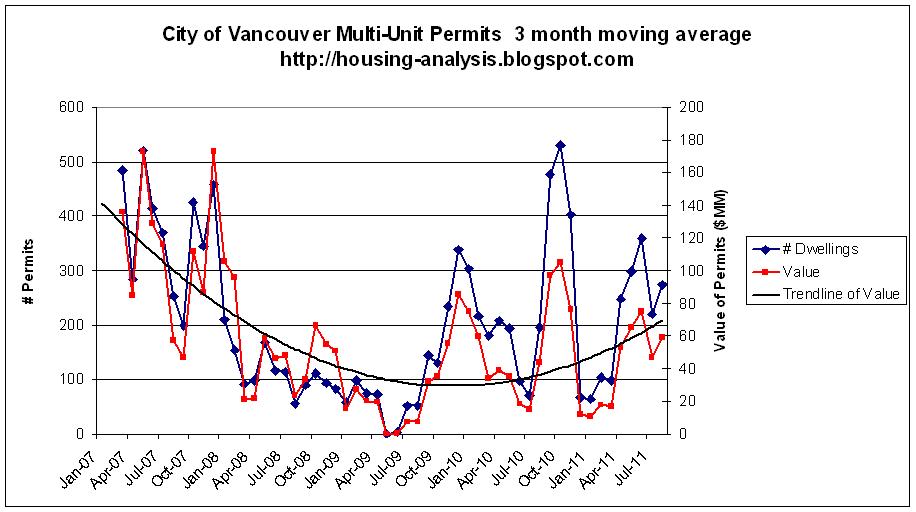

A long hiatus presenting CMHC data from the Vancouver area has ended and here are mohican/VHB's charts for housing starts, housing completions, and under construction, as well as graphs showing how they compare to population growth.

Analysis:

There was a severe, though brief, construction recession in 2008-2009, as indicated by the dropoff in starts. Note that since we are averaging 12 months of data, the troughs will be lagging by about 6 months (i.e. "group delay"). 12 months of completions look to have bottomed in July 2011, putting the actual bottom in about January 2011. The nadir of completions coincides with the start of a run-up in prices around that time.

Starts are climbing again; recent employment reports indicate robust construction employment, as we would expect as starts are booked and under construction trends up.

12 months of completions has been smoother than starts as projects are likely delayed rather than hurried. The amount of under construction between mid-2005 and mid-2009 indicates there was a significant backlog that has now been mostly worked through.

Despite higher prices and robust population growth from 2002-2011, new people per completion has averaged 2.1 as opposed to 2.8 from 1992-2001. This may be in part due to the change of construction mix -- more condos and less detached dwellings. At the same time, if detached houses have become larger than in previous decades, the number of bedrooms -- a potential method of determining total dwelling capacity -- may have increased in detached dwellings to partially offset the lower bedroom count in condos. As a start into this, I pulled the data from 2008-2011 on starts and completions by dwelling type (single detached and row/apartment/other) and graphed below. I then estimated 1.6 bedrooms per multi and 4 bedrooms per single-detached.

The dataset isn't large but one interesting point is that new single detached construction is trending down (i.e. starts < completions) whereas multi-unit construction is trending up. I was hoping to get a sense on how much of a lag the various construction methods produce; based on the graph it looks like detached construction starts lag completions by about 7 months. With less certainty it looks like the multi-unit construction minimum lags by about 19 months; this seems low so I hope I can get more data to fill this in.

The amount of under construction has increased above 12 months of starts starting in 2005. It is unclear why under construction has increased so significantly, though it could indicate increased speculative activity and favourable presale contract terms for developers -- the investors of the units under construction are willing to put up with longer project schedules or other delays. It may also be that multi-unit highrises have longer build times. This produces an interesting dynamic, namely that to accommodate future population growth estimates, larger projects must be more forward-looking.

To analyse this further I cross-correlated the 12-month starts and completions monthly data on 10-year forward sliding window and looked for peak correlation. The results indicate that under construction times are increasing, thus an increased time to build for new dwellings. This makes sense given that multi-unit construction is now taking a larger share of total construction, currently making up around 3/4 of all dwelling units. (If you go by my 4 bedroom 1.6 bedroom breakdown, that's an average of 2.2 bedrooms per dwelling, however multi would only compose 55% of new bedroom stock.)

In summary, new dwelling formation in the past decade has produced more dwellings per new entrant than in past decades. It is unclear how the condo-detached mix has contributed to allowing for a higher dwelling construction rate and how much is nascent oversupply. Further work breaking down starts by dwelling type by comparing to previous decades can help answer this. In addition, the concentration on dwellings with longer construction times may have implications for dwelling supply stability -- longer lags lead to more fluctuations in dwelling starts.