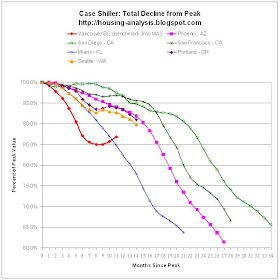

A quick update on GV benchmark compared to various US markets as tracked by the Case-Shiller HPI. I will show two graphs. One is the raw benchmark value the other is a 3 month moving average. The 3 month moving average (trailing -- this is not quite correct and I should be using balanced average as Thompson on RET pointed out but hey it is what it is) is probably a better comparison to Case-Shiller. But still, one can see the "spring bounce" is here. If you're buying on technicals, hey, throw in some moving averages to this graph and justify buying at today's values. Good luck with that. We'll have speaks in 2012.

Update

UpdateI have run the numbers comparing the Teranet HPI to the benchmark. In the short run, the Vancouver benchmark tracks Miami very well on the above graph, but even more surprising is that Toronto's HPI is falling faster than Vancouver's from peak, though Vancouver has fallen more in % terms. I will post the graphs in a subsequent post. We should not be surprised that the benchmark deviates from the HPI, though from what I have seen in the long run the two will eventually track each other reasonably well. It looks as if the benchmark has "overestimated" price drops but may now be "underestimating" them.

Why don't you use the Teranet data instead? Its method is very similar to Case Shiller...

ReplyDeleteThanks Jesse. Keep the faith everyone. It can't not happen here.

ReplyDeleteThis comment has been removed by the author.

ReplyDelete“Thanks Jesse. Keep the faith everyone.”

ReplyDeleteAhhhh, it's not about da numbers. It's about religion!

Michael, the Teranet HPI that is equivalent to the Case-Shiller HPI in the US is released several months after the fact. The benchmark tracks the HPI reasonably well over long time periods, with the added advantage of it being available days after month end.

ReplyDeleteI will put the Teranet HPI on the graph in a later post.

Now, off to do some yard maintenance. Ownership ain't free, but free labour certainly helps.

I appreciate the information and analysis provided by this blog- most of the other real-estate blogs have become juvenile.

ReplyDeleteMo, have you ever thought of plotting the absolute, monthly, cost of home ownership- taking into account the reduction in financing expense- in relationship to the 5% bounce back in Vancouver prices.

I think it would be interesting to find out if the jump in prices has actually raised the cost of ownership- from what it was at the beginning of the year. This might give some indication as to the resistance (and, support) level for prices in terms of actual monthly cash outflow.

Since, it seems that, most people make their financial decision from within the context of its affect on monthly cash flow: the direction of this graph might give us a view of the market that is more consistent with the paradigm of its participants- than prices or interest rates do in isolation.

As you have mentioned the price of ownership has drop by as much as 30% over the year.

The question then becomes: are the recent price increases completely absorbed by reduced financing costs- or, are they a sign of market strength in which the absolute cost of ownership is increasing.

Keep up the good work.

Thanks for the graphs Mohican and Jesse! This blog is the best one going. How about adding other Canadian cities to the decline charts to give a sense of national comparisons? Might give interesting perspective on the relative "easy money" availibility between Canada/US.

ReplyDelete"Now, off to do some yard maintenance. Ownership ain't free, but free labour certainly helps."

ReplyDeleteYou've bought I see :)

Econs question:

I heard inflation is already happening south of the border but hasn't reached the consumers yet. When it does, since Canada found a religion, it won't impact us much right?

I think it would be interesting to find out if the jump in prices has actually raised the cost of ownership

ReplyDelete...

Yes of course it has, because the average interest rate you pay over the life of the mortgage depends very little on when you buy. But the price does, a lot.

So many people don't think of this.

"You've bought I see :)"

ReplyDeleteThat's not what I said.

Yes of course it has, because the average interest rate you pay over the life of the mortgage depends very little on when you buy. But the price does, a lot.

ReplyDeleteWe've had declining interest rates for so long that it hasn't mattered if you thought of this because the interest rates have always gone lower. Now they can't go lower. I think there is a likelihood of of a snap back. The reversal of interest rate trend is going to bite extra hard for a long time because it's going to take a while before people get it.

This unfortunately is making this take a lot longer than anyone thought possible. A LOT of really bad decisions have been more than compensated for by interest rate drops not to mention price appreciation.

Your comment about the benchmark underestimating and overestimating price changes explains alot. I've been trying to understand how the benchmark can indicate that prices are rising/aren't dropping as fast considering all of the hard evidence of continued price drops, e.g. houses listed last year at $799K being listed today at $628K as well as the much larger number of houses in Van West and North Van below $850K compared to recent years.

ReplyDeleteFunshine, I will spend some time analysing the difference in methodologies of the benchmark and the Case-Shiller method.

ReplyDeleteQuickly, the Case-Shiller methodology looks at sales pairs of the same property and throws out outliers where it is obvious extensive renovations or rebuilds were performed (thus not a true apples-to-apples comparison).

The benchmark uses hedonics to give relative weights to a property's quantitative measures such as number of rooms, square footage, building age (?) and lot size, but does not, as far as I can ascertain, attribute anything to the "qualitative" measures such as neighbourhood, finish quality, views, or other features of a property that could bias up or down its sales price and are difficult to quantify in a spareadsheet.

Over time the benchmark will track the Case-Shiller methodology because qualitative measures of housing in Vancouver (rooms, square footage, etc.) is reasonably stable and quality improvements would bias both Case-Shiller and the benchmark equally.

But in the short term the benchmark can be biased if the sales mix changes such that the "qualitative" measures bias the "quantitative" measures to be higher or lower. For example perhaps "quality" properties are moving more now than they did last year so the benchmark price would be higher. The Case-Shiller accounts for this (insofar as quality is maintained through tenure) so would not be as affected by sales mix, though can be affected by properties whose quality has significantly improved but not enough to cause it to be discarded.

I do hear of bidding wars for some nicely renoed places where last fall they would sit idle, and some crack houses I see still sitting "idle" (in the sales sense). Who knows.

www.onlineuniversalwork.com

ReplyDeletewww.onlineuniversalwork.com

ReplyDelete